Missing one payment feels catastrophic, but the reality of how delinquent accounts work is far more layered than most people realize. Your credit score doesn't collapse the moment a payment slips past its due date. There's a timeline, a reporting process, and a set of rules that determine exactly when and how much damage occurs. Understanding this process gives you real power to act before things spiral. This guide walks you through what delinquency actually means, how it moves through stages, and the concrete steps you can take to protect and rebuild your credit.

Table of Contents

- What is a delinquent account?

- Stages of delinquency and credit reporting

- How delinquent accounts affect your credit score

- How long do delinquencies remain on your credit report?

- Delinquency trends and next steps for credit repair

- Why "one size fits all" advice on delinquencies fails

- Take control of your credit repair journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Definition of delinquency | A delinquent account is any account with a missed required payment, usually 30 days overdue. |

| Reporting stages matter | Delinquencies are reported in escalating stages and cause different levels of credit damage. |

| Score impact | Recent and repeated delinquencies have the greatest negative effect on credit scores. |

| Seven-year duration | Negative marks from delinquent accounts usually stay on credit reports for up to seven years. |

| Recovery is possible | With prompt action and the right strategy, you can minimize lasting damage and rebuild credit health. |

What is a delinquent account?

A delinquent account is simply a credit account where you've missed a required payment. That could be a credit card minimum payment, a monthly loan installment, or even a utility bill tied to your credit profile. The moment the due date passes without payment, the account is technically overdue. But here's what most people don't realize: being overdue for a few days is very different from being reported as delinquent.

Most creditors give you a short grace window before they act. The real damage begins when your account hits 30 days past due. That's the threshold at which lenders are allowed to report the late payment to the major credit bureaus. According to Capital One, a delinquent account is a credit account where a required payment is past due, typically after missing the due date or minimum payment. That definition sounds simple, but the consequences are anything but.

Common triggers for delinquency include:

- Missing a credit card payment entirely

- Paying less than the required minimum on a loan

- Skipping an auto loan or mortgage installment

- Failing to pay a medical bill sent to a creditor

- Ignoring a utility account tied to your credit

Delinquency is the first step on a path that can lead to default and eventually collections. The earlier you catch it, the easier it is to stop the damage.

Pro Tip: If you realize you'll miss a payment, call your creditor before the due date. Many lenders offer hardship programs or can defer a payment without reporting it as late.

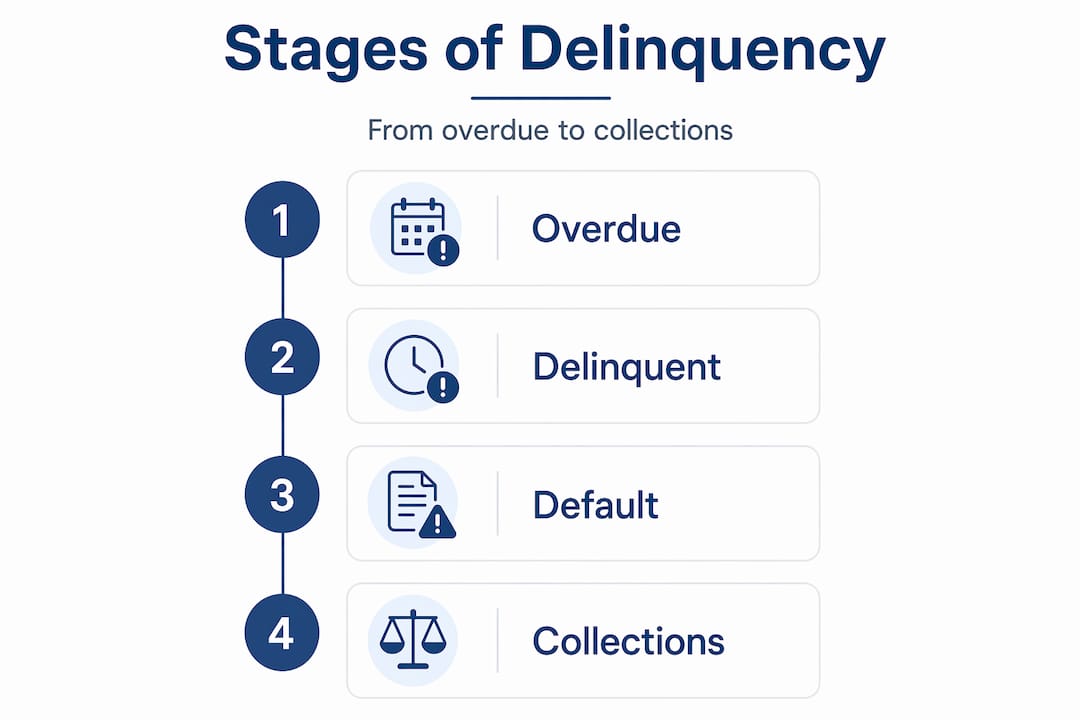

Stages of delinquency and credit reporting

The timeline of delinquency matters enormously. It's not a single event. It's a progression, and each stage creates a new negative mark on your credit report if the account stays unresolved.

Here's how the stages break down:

- 1 to 29 days late: The account is overdue, but creditors typically won't report it yet. You may face a late fee, but your credit score is still untouched.

- 30 days late: This is the first official reporting threshold. Your creditor can now notify the credit bureaus, and your score takes its first hit.

- 60 days late: A second negative mark is added. The damage compounds. Lenders begin to view you as a higher credit risk.

- 90 days late: At this stage, many lenders consider the account in default. This is a serious escalation with significantly greater consequences for your score.

- 120+ days late: The creditor may charge off the account or sell it to a collections agency. Both outcomes create additional negative marks.

As delinquency reporting stages show, the credit report impact is driven by lender reporting practices and the days-past-due stage, whether it's first reported at 30 days and how many subsequent updates occur. Not every lender reports at every interval, but many do, which means the longer you wait, the more entries stack up against you.

| Stage | Days past due | Reported to bureaus? | Credit impact |

|---|---|---|---|

| Overdue | 1 to 29 days | No | None |

| First delinquency | 30 days | Yes | Moderate drop |

| Second delinquency | 60 days | Yes | Significant drop |

| Default risk | 90 days | Yes | Severe drop |

| Charge-off or collections | 120+ days | Yes | Extreme damage |

Pro Tip: Even if you can't pay the full balance, making a partial payment before the 30-day mark can sometimes prevent a delinquency report. Always confirm with your lender what counts as a qualifying payment.

How delinquent accounts affect your credit score

Payment history is the single biggest factor in your credit score. It accounts for about 35% of your total score under most major scoring models. That means delinquencies hit you harder than almost anything else on your credit report.

The damage isn't uniform. Recency matters a great deal. A 30-day late payment from five years ago carries far less weight than one from last month. Lenders and scoring models treat recent delinquencies as a current warning sign, while older ones fade into the background over time.

"Delinquencies can hurt credit scores because payment history is a major scoring factor; scores are often affected by both the fact of delinquency and its recency and stage." — Discover

Here's a breakdown of how different delinquency levels affect your score:

| Delinquency type | Estimated score impact | Recovery timeline |

|---|---|---|

| 30-day late payment | 60 to 110 point drop | 9 to 12 months |

| 60-day late payment | 70 to 120 point drop | 12 to 18 months |

| 90-day late payment | 80 to 130 point drop | 18 to 24 months |

| Collections or charge-off | 100 to 150 point drop | 2 to 5 years |

These numbers vary based on your starting score. Someone with excellent credit often sees a larger initial drop because they have more to lose. Someone already in the fair range may see a smaller absolute drop but face a longer recovery road.

Key factors that amplify delinquency damage:

- Multiple delinquencies: Each one compounds the last. Two or three missed payments across different accounts can devastate a score faster than one severe delinquency.

- Account type: A mortgage delinquency generally signals more risk to lenders than a missed store credit card payment.

- Balance at time of delinquency: A large outstanding balance paired with a missed payment signals higher financial instability.

- Frequency of late payments: A pattern of repeated lateness is treated more harshly than a single isolated incident.

Understanding these nuances helps you prioritize which accounts to address first when you're working through a tough financial stretch.

How long do delinquencies remain on your credit report?

One of the most common questions people ask is: "Will this follow me forever?" The honest answer is no, but it will follow you for a while.

Most delinquencies stay on your credit report for seven years from the date of the first missed payment. That clock starts ticking from the original delinquency date, not from when you paid it off or when it was sent to collections. This is an important distinction because some consumers mistakenly believe that paying off a delinquent account resets the clock. It doesn't.

Key facts about delinquency timelines:

- The seven-year period is governed by the Fair Credit Reporting Act (FCRA), which sets limits on how long negative information can appear on your report.

- Once the seven years pass, the credit bureaus are required to remove the item automatically. You don't need to file a dispute for standard age-off removal.

- Paying off a delinquent account does not remove it early, but it changes the status from "unpaid" to "paid," which looks better to future lenders.

- The negative effect on your score typically weakens significantly after two to three years, even if the entry is still visible on your report.

- Certain types of negative information, like Chapter 7 bankruptcy, can stay on your report for up to ten years.

Statistic callout: Delinquent information typically remains on credit reports for up to seven years, with effects generally diminishing over time as the account ages and new positive information is added.

The practical takeaway here is that time is your ally if you stop the bleeding now. The sooner you resolve a delinquency and rebuild positive payment history, the faster your score will recover, even before the negative mark falls off entirely.

Delinquency trends and next steps for credit repair

You're not alone in dealing with this. Delinquency is a widespread issue, and understanding where you stand relative to broader trends can help you set realistic expectations for your recovery journey.

According to TransUnion's 2026 consumer credit forecast, 90-day delinquency rates for credit cards are projected to remain nearly flat, inching up by about 1 basis point to 2.57%. That tells us lenders are watching this space closely and that millions of consumers are navigating the same challenges you are right now.

"Serious delinquency rates are monitored closely by lenders and credit bureaus alike, and even small shifts can signal broader financial stress across consumer segments." — TransUnion 2026 Consumer Credit Forecast

Here's a structured path toward credit recovery after a delinquency:

- Get your current credit report. You can access your reports from all three major bureaus. Review each one carefully for accuracy, including the dates and amounts listed for any delinquencies.

- Identify the most recent and most severe delinquencies. These are the ones doing the most damage right now. Prioritize them.

- Contact your creditors directly. Many lenders have hardship programs, payment plans, or even goodwill adjustment policies that can help. Calling before a delinquency escalates is always better than calling after.

- Negotiate a pay-for-delete agreement if possible. Some creditors will agree to remove a delinquency from your report in exchange for payment. This isn't guaranteed, but it's worth asking.

- Dispute any inaccurate information. If a delinquency is reported incorrectly, such as the wrong date or amount, file a formal dispute with the credit bureau.

- Build positive payment history going forward. Every on-time payment you make from this point forward works to offset the negative marks already on your report.

Pro Tip: Set up automatic minimum payments on all accounts to prevent future delinquencies while you focus on catching up. Even a single on-time payment each month protects you from new damage.

Why "one size fits all" advice on delinquencies fails

Here's something the generic credit advice world rarely admits: the standard "just pay your bills on time" guidance is almost useless when you're already behind. It's like telling someone with a broken leg to walk it off. What you actually need is a strategy built around your specific situation.

The type of account matters. A delinquency on a secured auto loan behaves differently in terms of lender response and reporting frequency than one on an unsecured credit card. The lender's internal policies matter too. Some creditors report updates every 30 days like clockwork, while others batch their reporting monthly or quarterly. Knowing your lender's behavior can help you time your payments and negotiations more effectively.

Your financial goals matter just as much. If you're trying to qualify for a mortgage in the next 12 months, your strategy looks completely different than if you're simply trying to stabilize your score over the next few years. Rushing to pay off a charged-off account, for example, can sometimes restart activity on an old account and temporarily lower your score before it improves.

Understanding the delinquency stages explained in detail gives you the foundation to make smarter decisions rather than reactive ones. The consumers who recover fastest are the ones who treat credit repair as a process, not a panic response. They communicate with creditors, track reporting timelines, and build a realistic plan based on where their accounts actually stand, not where they fear they might be.

Sustainable recovery is built on understanding the nuances, not on chasing a quick fix that may not even apply to your situation.

Take control of your credit repair journey

If reading this has made you realize there's more to your credit situation than you thought, you're already ahead of most people. Knowledge is the first step, but action is what moves the needle.

At Credifixr, we built our platform specifically for people navigating delinquent accounts, collections, and the complicated process of credit recovery. Our tools help you manage delinquencies with structure and clarity, from identifying which accounts to tackle first to tracking disputes and monitoring score changes in real time. You don't have to figure this out alone. Explore our credit repair features to see how we support every stage of the recovery process, and visit Credifixr to get started with credit repair support tailored to your goals. Your credit story isn't finished. It's just waiting for the next chapter.

Frequently asked questions

How do I know if I have a delinquent account?

You have a delinquent account if you've missed a required payment and your lender has marked the account as late, which typically happens after 30 days past due. Checking your credit report from all three bureaus is the fastest way to confirm.

How badly does a delinquent account affect my credit?

Delinquencies can cause a significant drop in your credit score, especially when recent or severe, because payment history is a major scoring factor that makes up roughly 35% of your total score. The more recent and severe the delinquency, the greater the impact.

Can I remove a delinquent account from my credit report early?

Generally, delinquent accounts remain for up to seven years, but you may request removal if the information was reported in error or if you successfully negotiate a pay-for-delete agreement with your creditor.

What's the difference between delinquent and defaulted accounts?

A delinquent account is overdue but not yet in default; default generally means 90+ days late without payment, which triggers more severe consequences including potential charge-offs and collections activity.

Will paying off a delinquent account improve my score immediately?

Paying off the delinquency stops further damage and changes the account status to paid, but the late payment mark stays on your report for up to seven years with effects gradually diminishing as the account ages and positive history builds.