Your credit limit is not just a spending cap. It's one of the most direct levers you have to lower your credit utilization ratio, which is one of the biggest factors shaping your credit score. Learning to increase credit limit responsibly means knowing when to ask, how to ask, and what to do with the extra headroom once you have it. Done right, a responsible credit limit increase can improve your score, expand your financial flexibility, and signal to lenders that you're a borrower worth betting on.

Table of Contents

- Understanding credit limits and why they matter

- Preparing to request a credit limit increase

- How to request a credit limit increase responsibly

- Managing your credit after a limit increase

- Verifying results and planning future credit steps

- Why a cautious approach to credit limit increases pays off

- Manage your credit confidently with Credifixr

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand credit limits | Credit limits impact purchasing power and credit scores through utilization rates. |

| Prepare carefully | Wait 3-6 months and maintain low utilization before requesting increases. |

| Request responsibly | Use soft pull issuers if possible and request every 6 months with accurate info. |

| Manage post-increase | Avoid overspending by setting alerts and paying balances frequently. |

| Be patient | Frequent requests can hurt approval chances; consistency builds credit health. |

Understanding credit limits and why they matter

Your credit limit is the maximum amount your card issuer will let you carry on the card at any given time. But it does far more than set a spending ceiling. It directly shapes your credit utilization ratio, which is the percentage of available credit you're actually using. If you have a $2,000 limit and carry an $800 balance, your utilization is 40%. That's too high. Get that same $800 balance against a $4,000 limit and your utilization drops to 20%, which is a range most scoring models reward.

Credit limits influence utilization and, by extension, your overall creditworthiness. This is why a credit limit increase can lift your score without you paying down a single dollar of debt.

There are real upsides to a higher limit, but also real traps:

- Lower utilization can improve your credit score fairly quickly

- Greater purchasing power helps in emergencies or large planned expenses

- Better approval odds for future loans when your available credit looks healthy

- Risk of overspending increases when the ceiling feels farther away

- Debt accumulation can sneak up on you if you treat a higher limit as extra income

The most important thing to understand going in: a higher limit is a tool, not a reward. Used well, it helps you build credit. Used carelessly, it can set you back months of financial responsibility work.

Now that you know why credit limits matter, let's look at what you need to prepare before making a request.

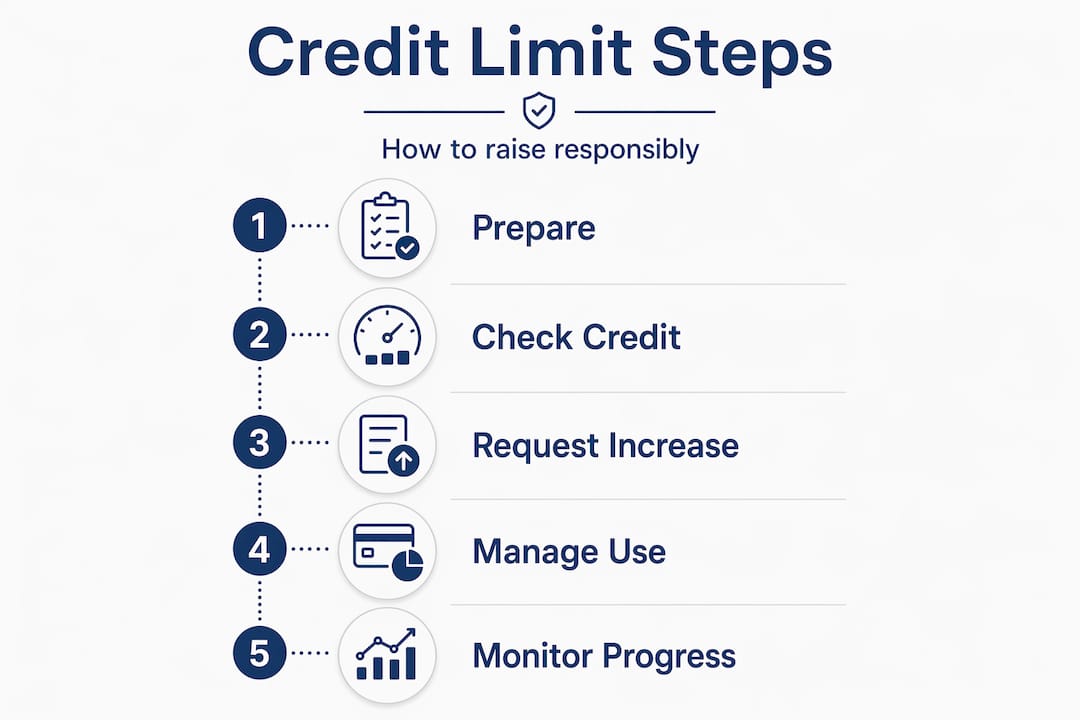

Preparing to request a credit limit increase

Most people skip this step entirely and just click "request increase" whenever the mood strikes. That's a mistake. Timing and preparation directly affect whether you get approved and whether the request helps or hurts your score.

A good payment history typically requires your account to be open at least three to six months before issuers seriously consider a request. New accounts almost always get declined.

Here's what to have ready before you request:

- On-time payment history: Even one missed payment in the recent past can tank your approval odds.

- Utilization below 30%: Issuers want to see you're not already maxing out what you have.

- Updated income information: Most applications ask for your total annual income. Don't forget side income.

- Employment status: Know whether you're full-time, self-employed, or part-time, and be accurate.

- Housing expenses: Rent or mortgage costs are often requested to assess your debt-to-income ratio.

| Factor | Ideal status before requesting |

|---|---|

| Account age | 6+ months |

| Payment history | Zero late payments in past 12 months |

| Utilization ratio | Under 30% |

| Income changes | Current and accurate |

| Last increase request | 6+ months ago |

Staying on top of these factors before you request puts you in the strongest possible position. If you want to work on staying financially responsible before applying, take the time to build that track record first.

Pro Tip: Pull your own credit report before requesting an increase. Look for errors or derogatory marks that could hurt your approval. Disputing inaccuracies first could meaningfully improve your position.

With preparation complete, let's explore exactly how to request an increase responsibly.

How to request a credit limit increase responsibly

The process itself is usually simple. Doing it in a way that protects your score takes a little more care.

Follow these steps for a responsible credit limit increase:

- Confirm the inquiry type. Before you submit anything, call your issuer or check their website to find out if they use a hard or soft pull for limit increase reviews. Many issuers use soft inquiries, which have zero impact on your score. Hard inquiries can temporarily lower your score by a few points.

- Log into your account or call customer service. Most major issuers let you request an increase online, through their app, or over the phone. The online or app route is usually fastest.

- Enter your updated income. Be thorough here. Total gross annual income can include wages, freelance income, investment income, and in some cases, a spouse's income if you have reasonable access to it.

- Request a 25% to 50% increase. Asking for double your current limit on the first try looks aggressive and often gets declined. A 25% to 50% bump feels realistic to underwriters and shows you've thought it through.

- Submit and wait. Some issuers approve instantly. Others take a few days. Avoid submitting multiple requests to different cards at the same time.

| Method | Speed | Inquiry type (varies by issuer) | Best for |

|---|---|---|---|

| Online/app | Instant to 24 hours | Usually soft pull | Most applicants |

| Phone | Same day | Soft or hard pull | Complex situations |

| In branch | 1 to 3 days | Varies | Relationship banking |

Pro Tip: If you get a counteroffer for a smaller increase than you requested, take it. A partial increase still lowers your utilization and sets you up for a larger ask in six months. Consistency in credit management builds toward the bigger wins.

After you submit your request, it's important to manage your credit behavior post-approval.

Managing your credit after a limit increase

This is where most people make mistakes. Approval feels like a win, and spending often follows. The data backs this up: 1 in 3 users increase utilization by 20% or more after a credit limit increase, which can reverse the score gains the increase created.

Here's how to protect yourself:

- Keep utilization below 30%, even though your limit is now higher. The goal is to use the new limit to lower your ratio, not fill it back up.

- Set spending alerts at 20% to 25% of your new limit. Most card issuers let you set these in their app. When you hit the threshold, you stop spending on that card.

- Pay your balance more than once a month. Credit card issuers report your balance to bureaus on your statement closing date. Paying mid-cycle keeps your reported balance low.

- Monitor your credit reports after the increase posts. Look for the updated limit and confirm your utilization has dropped.

- Treat the new headroom as a buffer, not a budget. The most credit-savvy people barely notice their limit went up. Their spending stays the same.

"A credit limit increase only helps your score if your balance stays the same or decreases. The moment you start spending to match the new limit, you've canceled the benefit."

This is what we mean by financial responsibility strategies. The increase is just the beginning. The real work is in how you behave after.

Finally, let's review how to verify your credit status and plan next steps.

Verifying results and planning future credit steps

A responsible credit limit increase doesn't end at approval. You need to confirm the change actually helped and build a plan for what comes next.

- Check your credit report within 30 to 60 days of the increase. Confirm the new limit is reported correctly to all three bureaus (Equifax, Experian, and TransUnion).

- Watch your score for movement. If your balance stayed flat but your limit went up, expect a score improvement within one to two billing cycles.

- Understand denials without overreacting. Denials often result from new accounts, missed payments, or too many recent requests. The letter you receive must explain the reasons. Use that information.

- Wait before reapplying. If you were denied, wait at least six months. Use that time to pay on time, reduce balances, and build the track record the issuer wanted to see.

- Explore new cards cautiously. If you've exhausted increases on your existing cards, a new card adds to your total available credit. But a new account also lowers your average account age, so weigh that tradeoff carefully.

| Situation | Recommended action |

|---|---|

| Approved, score improved | Maintain current habits, request again in 6 months |

| Approved, score unchanged | Check if limit updated correctly with all bureaus |

| Denied, payment history issues | Focus on on-time payments for 6 months |

| Denied, too many recent requests | Wait 6 months, avoid other credit applications |

| Denied, low income reported | Update income info, consider requesting a smaller increase |

With verification practices in place, here's a perspective worth considering before you make your next move.

Why a cautious approach to credit limit increases pays off

Here's the contrarian view most credit articles won't say directly: sometimes the best way to boost credit limit wisely is to not increase your limit at all.

If you have a history of spending to your limit, a higher ceiling doesn't fix the problem. It just raises the floor you'll fall from. The people who benefit most from a responsible credit limit increase are those who would have spent the same amount regardless. For everyone else, an increase can quietly accelerate the debt cycle they're trying to escape.

Frequent requests signal desperation to underwriters. The best results come from patience and consistent financial behavior, not from gaming the system every six months. One well-timed request made from a position of strength beats three aggressive asks made out of urgency.

The deeper truth here: your credit limit is a reflection of your financial behavior, not the other way around. When you prioritize on-time payments, keep balances low, and give your accounts time to age, issuers often raise your limit automatically without you asking. That's the goal. Automatic increases from issuers carry no inquiry risk and signal genuine trust.

Think of tips for raising your credit limit as a byproduct of doing the boring fundamentals well, not as a separate strategy to pursue. The readers who build the best credit over five to ten years are not the ones who knew all the tricks. They're the ones who paid on time, every time, and let the system reward them for it.

Manage your credit confidently with Credifixr

You've learned what it takes to increase credit limit responsibly, but knowing the steps and having the right tools are two different things.

Credifixr is built for people who take their credit seriously. With Credifixr's features, you can track your spending in real time, set utilization alerts so you never accidentally blow past 30%, and monitor your credit score for changes after a limit increase posts. Instead of checking manually and hoping for the best, you get a clear picture of where you stand and what to do next. If you're ready to take financial responsibility seriously, Credifixr gives you the structure to back it up.

Frequently asked questions

How often can I request a credit limit increase without hurting my credit score?

Wait at least six months between requests to minimize score impact and demonstrate sustained responsible use to your issuer.

Will requesting a credit limit increase always result in a hard credit inquiry?

Not always. Capital One uses soft inquiries that have no score impact, while other issuers may run a hard inquiry that causes a small, temporary dip.

What happens if my credit limit increase request is denied?

A denial does not affect your score directly. Review the denial letter for specific reasons, address those issues over the next few months, and reapply when your metrics are stronger.

How can I avoid overspending after my credit limit is increased?

Set alerts and pay twice monthly to keep your balance in check, and mentally treat your old limit as your new ceiling so the extra room stays in reserve.