Getting a call or letter from a debt collector can stop you in your tracks. Your heart races, your mind jumps to worst-case scenarios, and you may feel pressure to pay something you're not even sure you owe. Here's the thing: you have legal rights that most collectors count on you not knowing. A debt validation letter is one of the most powerful tools in your arsenal, and knowing how to write one correctly can pause collection efforts, protect your credit, and put you back in control of your financial situation.

Table of Contents

- Understanding debt validation letters and your rights

- What to prepare before writing your letter

- Step-by-step: How to write a debt validation letter

- After sending: Tracking, follow-up, and troubleshooting

- The uncomfortable truth about debt validation letters

- How Credifixr can help you take the next step

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Act quickly | You have 30 days after contact to dispute a debt and force validation, which pauses collection efforts. |

| Document everything | Track letters, timelines, and collector responses using certified mail and copies for your records. |

| Letters aren’t magic | A debt validation letter demands proof but does not erase valid debts or instantly fix credit reports. |

| Choose the right strategy | Use validation for proof from collectors, but dispute credit report errors directly with bureaus. |

| Support is available | Professional tools and expert help can simplify managing and disputing debts when things get complex. |

Understanding debt validation letters and your rights

A debt validation letter is a written request you send to a debt collector demanding proof that a debt is legitimate, that the amount is accurate, and that the collector has the legal right to collect it. This right is grounded in the Fair Debt Collection Practices Act (FDCPA), a federal law that governs how third-party collectors can contact you and what they must do when you challenge a debt.

Under the FDCPA, you have the right to request verification of any debt a collector contacts you about. Once you send that request, the collector must stop all collection activity until they provide written verification. This is not a loophole. It is a legal obligation they cannot ignore.

"A consumer dispute letter should clearly state you don't owe all or part of the money, request verification, and be sent promptly; it is not an admission of liability."

That last part matters enormously. Sending a validation letter does not mean you are agreeing that you owe the debt. You are simply exercising your right to see the evidence.

Key rights you hold under the FDCPA:

- The right to request written verification of the debt

- The right to have collection activity paused while verification is pending

- The right to know the name and address of the original creditor

- The right to dispute the debt without it being treated as an admission of liability

- The right to report violations to the Consumer Financial Protection Bureau (CFPB)

Timing is critical. The 30-day dispute window begins from the date of first contact. If you act within that window, the collector is legally required to stop collection attempts until they send you written verification. After 30 days, you can still dispute the debt, but the collector is not required to pause collection while they respond.

What a debt validation letter can and cannot do:

| What it CAN do | What it CANNOT do |

|---|---|

| Pause collection activity legally | Erase a legitimate debt |

| Force the collector to provide proof | Remove items from your credit report automatically |

| Protect you from liability admission | Stop lawsuits already in progress |

| Expose invalid or expired debts | Guarantee the collector will comply |

| Buy you time to review your options | Substitute for a credit bureau dispute |

Understanding these boundaries is what separates people who use this tool effectively from those who feel disappointed when the letter alone does not solve everything.

What to prepare before writing your letter

Once you grasp your rights and the purpose of the debt validation letter, it is time to organize everything you will need to act confidently. Rushing into writing the letter without the right materials can weaken your position and create gaps in your records.

Documents and information to gather:

- The original collection notice or letter from the collector

- Any previous statements or bills related to the debt

- Records of prior payments, if applicable

- Your account number as listed on the collection notice

- The collector's full name, address, and contact information

- Any notes from phone calls, including dates and what was discussed

One of the most important steps you can take is to keep copies and records of every communication you have with the collector. This creates a paper trail that protects you if the situation escalates or if you need to file a complaint.

Why certified mail matters:

Sending your letter by certified mail with return receipt requested is not just a formality. It gives you a legally recognized timestamp showing when the collector received your letter. If they later claim they never got it or dispute the timeline, your certified mail receipt is your proof. Regular first-class mail offers no such protection.

The 30-day rule in practice:

Imagine you receive a collection notice on January 1st. You have until January 31st to send your dispute letter and trigger the full legal protections of the FDCPA. If you send it on February 5th, you can still dispute the debt, but the collector is not required to halt collection while they respond. That six-day difference can change the entire dynamic of your situation.

Pro Tip: Create a dedicated folder, either a physical one or a digital folder on your computer or phone, to store every document related to this debt. Label it with the collector's name and the date of first contact. This simple habit can save you hours of scrambling later and makes your case much stronger if you ever need to escalate.

Quick preparation checklist:

| Item | Why it matters |

|---|---|

| Collection notice | Identifies the debt and collector details |

| Account records | Helps verify or dispute the amount claimed |

| Prior payment records | Shows history and may reveal errors |

| Certified mail supplies | Creates legal proof of delivery |

| Calendar reminder | Tracks the 30-day window and response deadlines |

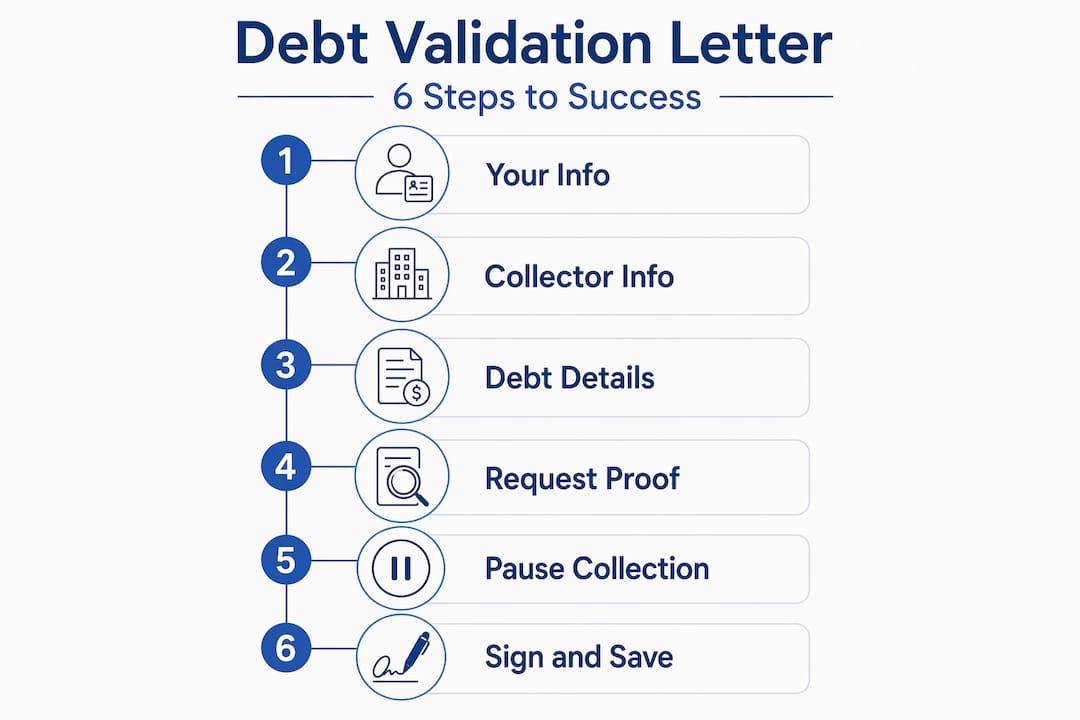

Step-by-step: How to write a debt validation letter

After collecting your materials, you are ready to write. Follow this step-by-step blueprint to craft a letter that stands up for your rights without accidentally working against you.

Step 1: Add your identifying information

At the top of the letter, include your full name, current mailing address, and the date. If the collection notice references an account number, include it here as well. This helps the collector match your letter to the correct account.

Step 2: Add the collector's information

Below your details, write the collector's full name and mailing address exactly as it appears on their notice. Accuracy here prevents any claim that your letter was sent to the wrong party.

Step 3: State your dispute clearly

This is the heart of the letter. You need to clearly communicate that you are disputing the debt. A dispute letter should clearly state you don't owe all or part of the money and request verification. Here is a sample statement you can adapt:

"I am writing to dispute the debt referenced above. I do not acknowledge that I owe this debt and I am requesting written verification of the debt as required under the Fair Debt Collection Practices Act, 15 U.S.C. § 1692g."

Step 4: Request specific information

Do not leave the collector guessing about what you need. Ask for:

- The name and address of the original creditor

- The amount of the debt and how it was calculated

- A copy of any agreement that created the debt

- Proof that the collector is licensed to collect in your state

- Documentation showing the chain of ownership if the debt was sold

Step 5: Demand collection activity stop

State clearly that you expect all collection efforts to cease until they provide written verification. This puts your request on record and reinforces your FDCPA rights.

Step 6: Close professionally

Sign the letter with your printed name. Do not sign with a handwritten signature that could be copied and used on other documents. Keep the tone firm but professional throughout.

Pro Tip: Save a dated digital copy of the letter before you seal the envelope. Take a photo of the envelope and the certified mail receipt as well. If any dispute arises about what you sent or when, these records are your best defense.

After sending: Tracking, follow-up, and troubleshooting

Knowing how to send your letter is just the start. Effective resolution depends on what you do next and how you respond to what the collector does or does not do.

Confirming delivery and tracking deadlines:

Once you send the letter, log the certified mail tracking number and check delivery confirmation online. Note the exact date of delivery. From that point, the collector has a reasonable window to respond with verification. Mark a follow-up date on your calendar, typically 30 to 45 days out, to review whether they have responded.

What collectors can and cannot do after receiving your letter:

- They cannot continue collection calls or send additional demand letters

- They cannot report the debt as delinquent without noting it is disputed

- They can send you written verification of the debt

- They can choose to stop collecting and close the account

- They cannot threaten legal action as a pressure tactic during the dispute window

Common follow-up scenarios:

Scenario 1: The collector sends verification. Review the documents carefully. If the debt is valid and the amount is accurate, you will need to decide how to proceed, whether that means negotiating a settlement, setting up a payment plan, or seeking professional guidance.

Scenario 2: The collector goes silent. If you receive no response, the collector cannot legally resume collection activity. Document the silence and consider filing a complaint with the CFPB.

Scenario 3: The collector ignores the dispute and keeps calling. This is a violation of the FDCPA. Document every contact, including dates, times, and what was said. You may have grounds for legal action.

You can explore validation letter outcomes in more detail to understand what each scenario means for your credit and your next steps.

When to use a credit bureau dispute instead:

This is a point many people miss. If your real concern is an error on your credit report, such as a debt that was never yours, a balance that is wrong, or a duplicate entry, a debt validation letter sent to the collector is not enough. The FCRA credit-bureau dispute process is the correct route for credit reporting inaccuracies. Similarly, validation letters require collector proof but do not automatically erase credit report items. These are two separate processes, and you may need to pursue both.

Pro Tip: Mark every deadline and response in a dedicated calendar or app. Set reminders three days before each deadline so you have time to act, not just react. Missing a follow-up window can cost you important legal protections.

The uncomfortable truth about debt validation letters

Here is something most guides will not tell you directly: debt validation letters are powerful, but they are not magic. We have seen many people send a letter, feel a rush of relief, and then wait for their credit problems to disappear on their own. That is not how this works.

Validation requests pause collection and require proof, but they do not automatically fix credit reports. A debt that is validated and legitimate will still sit on your credit report. The collector, once they provide verification, can resume collection activity. And if you have multiple debts in collections, one letter to one collector only addresses one piece of a larger puzzle.

The effects on credit reporting can be complex, and understanding them requires looking at the full picture of your credit profile, not just a single account.

What actually works is a layered approach. Start with the validation letter to protect yourself immediately. Then assess whether the debt is legitimate. If there are reporting errors, file credit bureau disputes under the FCRA. If the debt is real but unmanageable, explore negotiation or professional credit repair support. No single letter solves a credit problem that took months or years to develop.

The consumers who come out ahead are the ones who treat debt validation as step one in a process, not the entire solution. They stay organized, they follow up, and they use every tool available to them, not just the first one they learn about.

How Credifixr can help you take the next step

If you are ready to take control of your credit beyond sending a single letter, consider getting full support for your financial journey.

Managing multiple debts, tracking disputes across several collectors, and navigating credit bureau processes at the same time can feel overwhelming. The Credifixr platform is built specifically for people in exactly this situation. Whether you need help organizing your disputes, understanding what is on your credit report, or accessing tools that make the process less stressful, Credifixr offers complete credit repair support designed to move you forward. You can also explore invoice management features that help you stay on top of your financial obligations. Taking one step at a time, with the right tools behind you, makes all the difference.

Frequently asked questions

What is the main purpose of a debt validation letter?

It forces the collector to provide evidence that the debt is legitimate and pauses collection efforts until written verification is provided to you.

Does a validation letter remove a debt from my credit report?

No. It compels the collector to verify the debt, but credit report items require separate disputes filed directly with the credit bureaus under the FCRA process.

What should I do if I suspect identity theft or inaccurate reporting?

Dispute the item directly with the credit bureau using the FCRA dispute process, rather than relying solely on a debt validation letter sent to the collector.

Is it necessary to send a validation letter by certified mail?

Certified mail is strongly recommended because it provides proof of delivery and documents the exact timeline, which is critical for enforcing your legal protections.

What happens if a debt collector ignores my validation letter?

Collectors cannot legally pursue collection until they provide validation. If they continue anyway, document every contact and dispute within the 30-day window to preserve your rights, then consider reporting the violation to the CFPB or seeking professional assistance.